Instrument data staging and DQA

From the Staging and Analysis tab of the Instrument Data Mart page, you can copy financial instrument data to the staging table before processing of Data Quality Analysis (DQA). You can also configure DQA settings.

NOTE: The staging table is the source for processing of Funds Transfer Pricing (FTP) and for the cash flow data generated for planning.

This tab includes the following sub-tabs:

Populate Staging Table sub-tab

From this sub-tab, you can populate the staging table for DQA and then run DQA.

TIP: You can also process DQA separately after the staging table is populated. For example, if you process DQA with a setting disabled that you had intended to enable, you can rerun DQA without reloading the staging table.

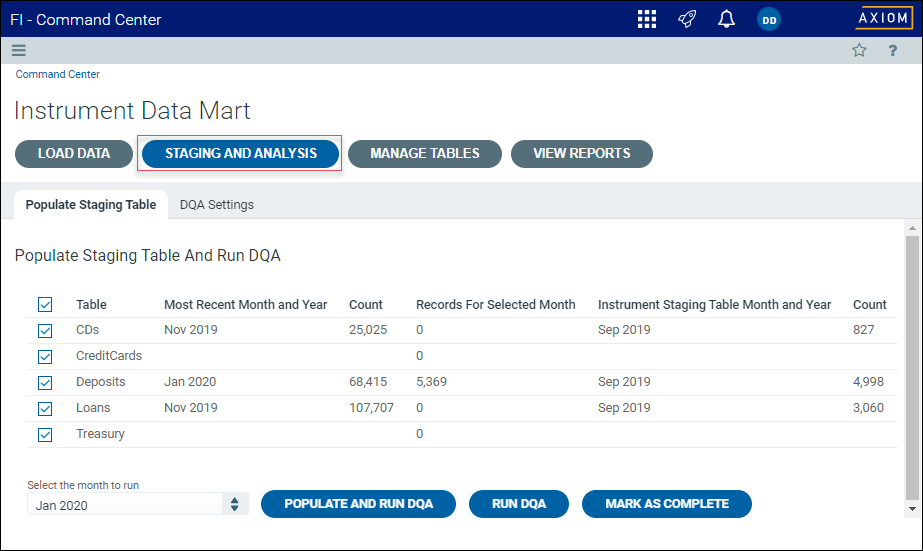

The table on this sub-tab contains the following information.

| Column | Description |

|---|---|

| Table | Lists the available instrument source tables for specific types of financial instruments, which includes certificates of deposit (CDs), credit cards, deposits, loans, and treasury assets. |

| Most Recent Month and Year | Lists the most recent month and year for which instrument data is available for the specified type of financial instrument. |

| Count |

Lists the number of financial instruments of the specified type in the table. |

| Records for Selected Month | Lists the number of data records for the month listed under Most Recent Month and Year. |

| Instrument Staging Table Month and Year |

Lists the month for which the staging table was most recently populated. |

| Count | Lists the number of financial instruments of the specified type in the processed table. |

Populating the staging table

To populate the staging table for DQA:

-

On the Staging and Analysis tab, click the Populate Staging Table sub-tab if it is not already selected.

-

Under Populate Staging Table and Run DQA, select the month for which to populate tables from the Select the month to run drop-down list.

-

Click Populate and Run DQA.

-

In the Submitted for Processing dialog, click OK.

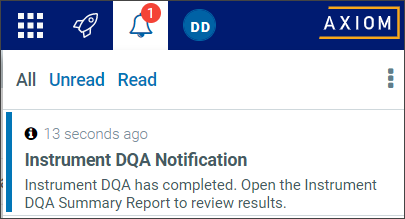

Running DQA on populated staging tables

To run DQA on staging tables that have been populated:

-

When the Axiom FI web client displays a numbered red icon indicating pending notifications, in the list of notifications, click Instrument DQA Notification.

Click to enlarge image

-

On the Populate Staging Table sub-tab, click Run DQA.

-

In the Submitted for Processing dialog, click OK.

Marking a populated table as complete

To mark a populated table as complete after DQA:

-

When the Axiom web client displays a numbered red icon indicating pending notifications, in the list of notifications, click Instrument DQA Notification.

Click to enlarge image

-

On the Populate Staging Table and Run DQA page, click Mark as Complete.

-

In the Mark as Complete dialog, click OK.

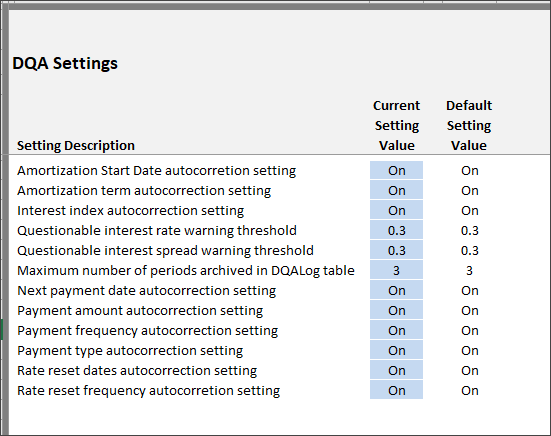

From this sub-tab, you can modify settings stored in the DQASettings table in the Axiom desktop client. These settings support optional correction of data about financial instruments.

The following table summarizes how each setting is applied in the DQA process. When either the Cash Flow Forecaster (CFF) model or the FTP model is present in your system, the data correction is applied to that model.

| DQA Setting | Description | Valid Values | Model Where Correction Applied |

|---|---|---|---|

| Amortization start date | Verifies the first amortization date falls on or after the origination, or renewal, date. If an error is detected, DQA sets the date to one payment period after the origination or start date. | On, Off | CFF, FTP |

| Amortization term auto correction setting | Automatic correction of AX_AmortTerm. Default value is On. | On, Off | CFF, FTP |

| Interest index auto correction setting | Automatic correction of AX_IntIndex. Default value is On. | On, Off | CFF only |

| Questionable interest rate warning threshold | Warning threshold for questionable interest rates. Any AX_IntRate value greater than the threshold setting triggers a DQA warning message. Default value is 0.3. | 0.0 to 1.0 | CFF, FTP |

| Questionable interest spread warning threshold | Warning threshold for questionable interest spreads. Any absolute AX_IntSpread value greater than the threshold setting triggers a DQA warning message. Default value is 0.3. | 0.0 to 1.0 | CFF only |

| Maximum number of periods archived in DQALog table | Controls the maximum of historical DQA results that will be stored in the DQALog table. Default value is 3. | 1 to 6 | CFF, FTP |

| Next payment date auto correction setting | Automatically corrects AX_NextPmtDate. Default value is On. | On, Off | CFF only |

To configure DQA settings:

-

On the Staging and Analysis tab, click the DQA Settings sub-tab if it is not already selected.

-

Under View or Edit DQA Settings, click Open.

NOTE: The DQA Settings utility opens in the Axiom desktop client.

-

In the DQA Settings utility, edit settings in the blue fields as needed.

Click to enlarge image

TIP: The utility displays default settings when first opened. Only settings in blue fields can be edited. All other fields are read-only.

IMPORTANT: The only configurations that can be changed in DQA are the DQA settings controlled by the DQA Settings utility. Do not attempt to modify any other component of DQA, especially Structured Query Language (SQL) logic.

-

When done editing, close the utility.

DQA correction of instrument data

DQA identifies, and where possible, corrects bad loan and CD data that can cause errors in Axiom’s Cash Flow Forecaster (CFF), FTP Cash Flow, and FTP Term to Maturity models. DQA analyzes only the data points that are essential to the proper function of these models.

When instrument records contain problematic data that cannot be corrected, DQA flags those records as “failed.” Within each model, a failed instrument record is processed differently than a passing or automatically corrected record.

- For CFF, this means that the record is processed by the model, but the model does not project future cash flows.

- For FTP, the models assign the default FTP rate rather than a strip-funded FTP rate or a term-to-maturity FTP rate.

DQA performs the following corrections automatically.

-

DQA sets the non-maturity flag value to 1 (TRUE) when AX_MatDate (maturity date) is null or blank. Otherwise, DQA sets the non-maturity flag value to 0 (FALSE).

NOTE: DQA makes its own assignment of non-maturity flag values regardless of what the client provides. If the client data import uses the exact same logic as DQA, then non-maturity flag values are the same after DQA as before DQA, and DQA assigns an event code of 0 (pass).

-

Axiom calculates its own maturity term as the number of months between the greater of either AX_OrigDate (origination date) or AX_RenewalDate (renewal date), when renewal date is less than the as of date, and AX_MatDate (maturity date).